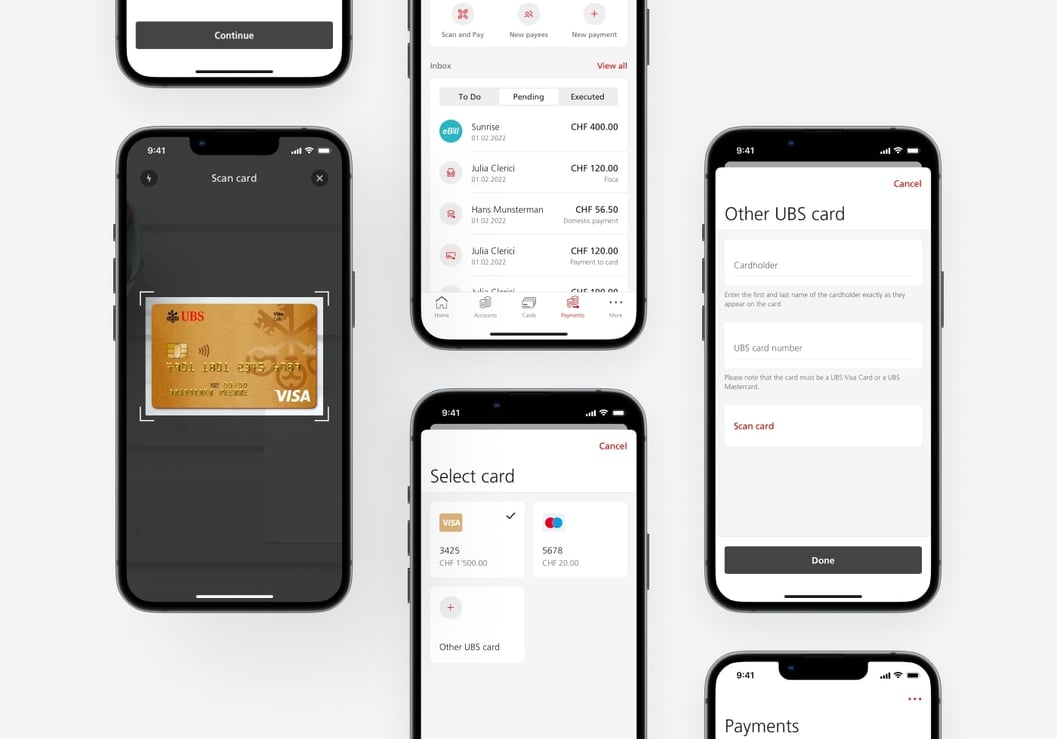

Mobile-first: Supporting UBS designers in banking app redesign

UBS, a financial and banking leader on the global market, teamed up with Netguru to build a best-in-class mobile banking app by achieving more consistent payment flows, shorter login process, easier in-app navigation, and seamless experience across app features.

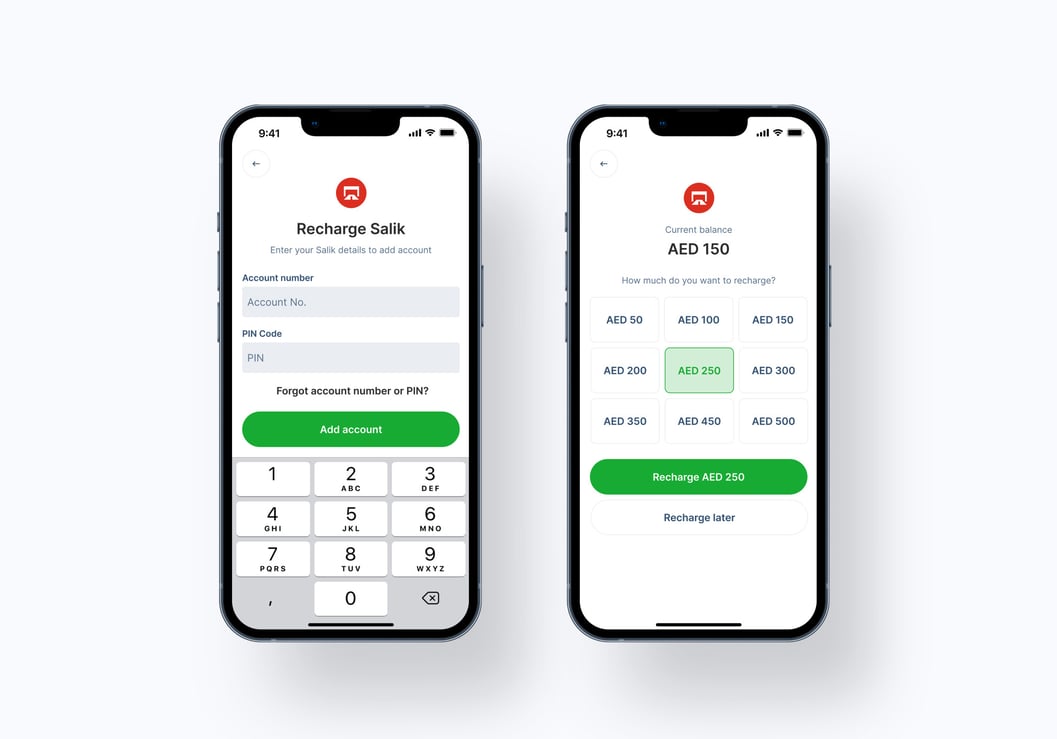

Our mobile-first approach resulted in:

- A new user-centric home screen that provides data about the client's financial health

- Improved loading behavior and error handling

- Redesigned payment and login features for a smoother user experience

- A native design approach and a new process for improving existing components and adding new ones to the library

.jpg?width=50&height=50&name=Krawczy%C5%84ski%20Mateusz%201%20(1).jpg)

%20(1).jpg?width=384&height=202&name=tablet%20and%20flowers%20(1)%20(1).jpg)