Fintech App Development Services - Overview

In the dynamic realm of finance, where speed and efficiency are paramount, both businesses and consumers are on a quest for innovative solutions that simplify, secure, and supercharge their financial management.

This is where fintech app development services comes in, crafting a new era of financial applications that are not only secure but also user-friendly and feature-rich.

What is fintech app development?

In the financial sector, fintech software solutions emerge as the champions. These versatile fintech app solutions fuel a myriad of critical services, from seamless mobile banking experiences and robust payment gateways to sophisticated investment platforms.

Behind these innovations lies the prowess of a fintech app development team, armed with a diverse array of cutting-edge technologies. Together, they craft mobile and web applications that rise to meet the distinctive challenges faced by banks, financial institutions, and the entire fintech landscape.

UX design for fintech applications

A fintech app’s success largely depends on its ability to offer a seamless, user-friendly experience.

This is where UX design comes into play, focusing on crafting intuitive and engaging interfaces that allow users to navigate the app with ease, whether they’re checking their account balance, making a payment, or monitoring their investments.

Custom fintech development

In an increasingly competitive financial landscape, businesses require tailored fintech solutions that cater to their unique needs and objectives. Custom fintech app development companies provide just that, offering mobile and web applications designed to address specific business requirements, as well as seamless integration with existing systems.

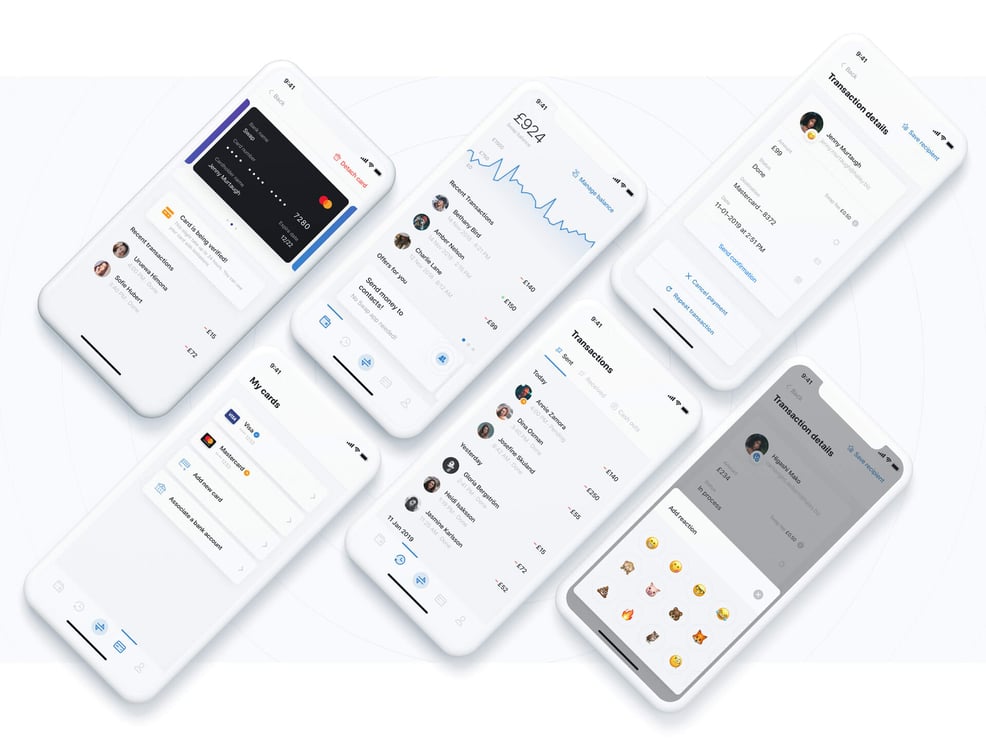

Web & mobile fintech app development

In the dynamic realm of fintech, the catalyst for innovation lies in mobile and web applications. They serve as the driving force, seamlessly connecting you to a world of financial services and products, accessible anytime and anywhere, across all your devices.

Envision a future where mobile banking apps grant you immediate control over your accounts, simplifying tasks such as bill payments and money transfers with effortless precision. Think of investment apps that provide you with real-time insights, equipping you to make informed decisions, regardless of your location or schedule.

%20(1).jpg?width=384&height=202&name=tablet%20and%20flowers%20(1)%20(1).jpg)